Credit risk: mortgages 2022

Supervised institutions incur a two-pronged credit risk when they grant a mortgage: Firstly, there is the risk of the customer not being able to meet the interest and repayment obligations, resulting in a credit default for the lending institution. Secondly, there is the risk that the value of the property serving as collateral will fall at the point of default, thereby entailing losses. The better the affordability, the lower the risk of default. The risk of a large loss in the event of default increases if property prices collapse in a crisis. This risk can be minimised if the loan-to-value ratio is not excessively high and borrowers are required to provide sufficient own funds. Guidelines for the loan-to-value ratio are provided in the banking sector’s self-regulation. The corresponding rules for the financing of investment property were tightened as of 1 January 2020. There are no binding quantitative rules for affordability.

Affordability risks have increased in the last four years for newly granted mortgages for financing both owner-occupied housing and residential investment properties. On the one hand, this is because less stringent affordability calculations were accepted in both segments. For example, in the context of on-site supervisory reviews or enquiries to the supervised institutions, FINMA observed that looser lending criteria were being applied in some instances. On the other hand, the proportion of variable-rate mortgages has risen significantly due to the sharply increased interest rates for long terms. This, in turn, increases the affordability risks.

The lending values remained stable for new financing arrangements for owner-occupied housing in recent years. The proportion of residential investment properties with a high collateral value has fallen due to the tightened self-regulation guidelines.

Overall, the volume of mortgage loans has continued to increase, but somewhat more slowly than in the previous year. Due to the recovery of the economy after the pandemic, the relation between mortgage loans and gross domestic product has not increased further for the first time since 2008/09. There has been a continuous fall in the proportion of financing arrangements for buy-to-let properties since the third quarter of 2021, presumably because mortgage interest rates have increased significantly since then, particularly for longer terms.

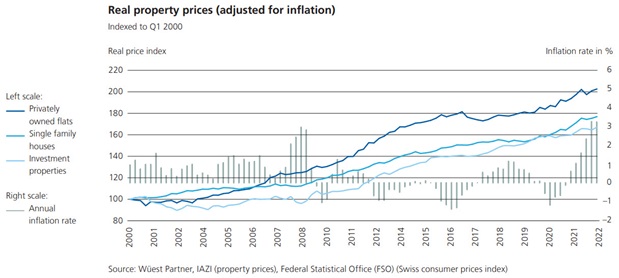

In the owner-occupied housing segment, growth momentum has recently slowed down somewhat. The sharply increased financing costs ought to have a dampening effect on demand for mortgage loans. However, due to the scant offer of property available to purchase, there is still significant excess demand, meaning that the prices adjusted for inflation have also continued to rise (see figure labelled “Real property prices”). This is an indication of overheating

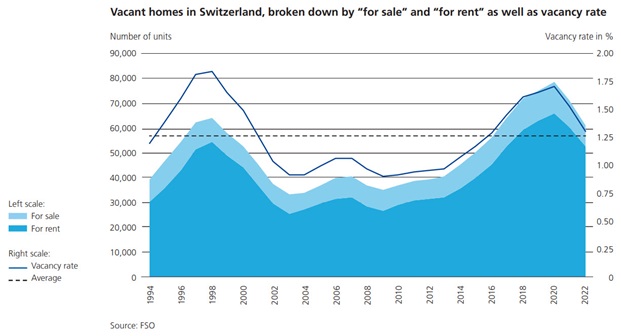

Prices in the residential buy-to-let market have also been rising significantly again following a sideways trend from the beginning of 2021 to mid-2022, which is also confirmed in the prices adjusted for inflation (see figure labelled “Real property prices”, top left). Because high immigration levels drive up rental demand and supply is declining, quoted rents have increased again. At the same time, vacancy rates have also dropped once more (see figure labelled “Vacant homes in Switzerland”, bottom left). The associated increase in returns from rental income fosters the demand for residential investment properties on the part of investors despite increased mortgage interest rates. The user and investor markets are developing in parallel again for the first time in years and the increased prices can be justified by demand. However, the end of the negative interest rate era opens up new investment alternatives. The surge in building material prices also ought to have a dampening effect on development projects and thus on supply.

The consequences of a real estate crisis would be significant for the Swiss financial centre. If real estate were to be devalued, loans would be covered to a much lesser degree than was assumed when they were granted. This would result in losses for the lending institutions. Stress tests carried out by FINMA show that a real estate crisis involving sharp price corrections could lead to losses in double-digit billion territory. In the event of a severe real estate crisis, some banks would have too little loss-absorbing capital held for the mortgage portfolio to bear the corresponding losses. In view of the high overall volume of mortgage lending, capital held by the banks is of great importance. At the request of the Swiss National Bank and following consultation with FINMA, the countercyclical capital buffer was reactivated at the end of September 2022. This increases the capital buffer of the lending banks.

(From the Risk monitor 2022)