Correction in the real estate and mortgage market 2021

Negative interest rates pose a risk of bubbles developing in various asset classes, particularly in the real estate market. In the investor market, property remains coveted as an investment, as it at least promises positive returns in a persistently low interest rate environment. Due to the declining demand for commercial and office premises as a result of the coronavirus pandemic, investors are focusing their attention even more strongly on the residential property segment. This is subjecting residential property prices to upward pressure. Demand in the user market has remained stable over the reporting period. However, there is evidence of a shift in demand towards larger apartments, a phenomenon triggered by the surge in working from home during the pandemic. Vacancies have declined recently in both the rental and ownership segments. On the one hand, net immigration has remained high due to the fall in the number of people emigrating during the pandemic, while on the other construction activity has declined. Risks have not increased in the residential property sub-market as a result. However, it is too early to call a trend reversal in the user market.

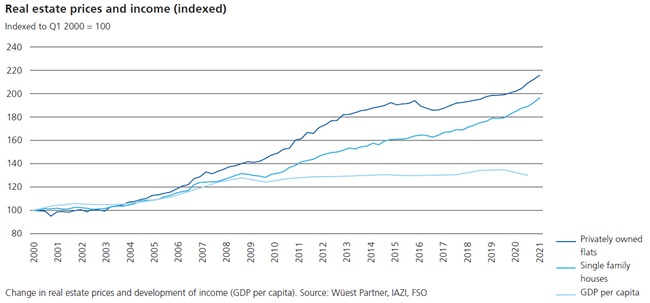

The price of owner-occupied housing has once again risen strongly since the outbreak of the coronavirus pandemic, namely by some 6% annually (see graph). The pandemic has increased the importance of the home, particularly as working from home allows employees to consider property purchases further away from the workplace. The demand for home ownership has increased as a result, and has been additionally spurred by record-low mortgage interest rates. Supply has been scarce for years, which has further fuelled price growth. But this price momentum has further increased the divergence between property prices and incomes, which suggests a bubble is building.

Whereas economic output slumped during the coronavirus crisis, mortgage volumes increased further. As a result, the mortgage debt to GDP ratio in Switzerland has increased further. Total debt as a proportion of economic output has been increasing for years, which increases risks in the system. On the other hand, the intensification of self-regulation by the Swiss Bankers Association – which took effect on 1 January 2021, and is considered by FINMA as the minimum standard – has had some impact. For example, the risk profile with regard to the loan-to-value ratio of newly granted mortgages for investment properties has improved. In other words, the size of the average new mortgage granted has decreased in relation to property prices. Analysis of the risk profile of existing mortgages is not possible, however, as the corresponding data is lacking. Moreover, the self-regulation guidelines do not apply to the “buy-to-let” segment hence the risk profile here is likely to be higher.

The development of newly granted mortgages continues to exhibit increased affordability risks. In the area of outstanding mortgage loans, the data required to undertake an appraisal of financial stability risks in the mortgage market and an improvement in prudential oversight is lacking. One macroprudential instrument in this area is the countercyclical capital buffer (CCyB), which increases the banks’ freedom of manoeuvre and resilience in a crisis. The CCyB counteracts imbalances in the mortgage and real estate market. It is currently suspended, but can be reactivated by the Federal Council subject to an application from the Swiss National Bank following consultation with FINMA.

The consequences of a real estate crisis would be significant for the Swiss financial centre. Stress tests carried out by FINMA show that a real estate crisis involving sharp price corrections could lead to losses in double-digit billion territory, with the result that just under half of the banks in the random sample would no longer fulfil minimum capital requirements. As mortgages are the most important pillar of business for the majority of banks, this would have significant consequences for financial stability. Insurers too would suffer painful losses in their mortgage and real estate portfolios in the event of a real estate crisis. In addition, liquidity measures and a need to reduce risk could force insurers to sell off real estate investments. This would have the effect of further intensifying the slump in property prices. For real estate funds, price corrections would entail valuation losses and the resulting fund outflows, which could in turn trigger liquidity problems.

(From the Risk monitor 2021)