Mortgage market measures 2018

While the price increase of owner-occupied residential property appears set to stabilise at a high level, the strong market momentum in the investment property market continues unabated. Some regions of Switzerland are currently experiencing major excess supply in the market for rental apartments. By mid-2018 the number of vacancies published by the Federal Statistical Office had reached its highest level since 1999. Once more, the risk has increased over the previous year, due to the continued construction activity and persistent attractiveness of property as an investment. This market development is particularly significant for the banking sector. Insurers, pension funds and other loan providers outside the banking sector only account for a comparatively minor share of the mortgage market ( below 6%).

Investment properties particularly exposed

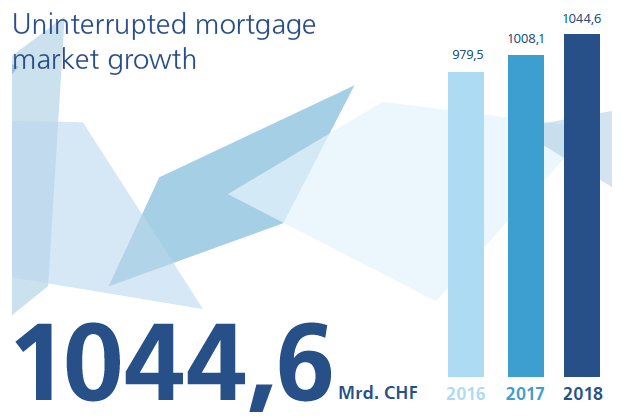

The mortgage volume held by Swiss banks has doubled over the past 15 years and amounted to CHF 1,044.6 billion at the end of 2018. Institutions with significant mortgage exposure to the investment property sector (which has a higher loan-tovalue ratio) would be directly affected by an abrupt fall in prices. The valuation of an investment property depends on the associated returns and the capitalisation rate. The latter moves in line with the interest rate. When the interest rate rises, the capitalisation rate has to be revised upwards, leading to lower property valuations. Vacancies also reduce the value of an investment property due to the lower rental income. A lower valuation increases the loan-to-value ratio of a property. Those properties that already have a relatively high loan-to-value ratio undergo the risk of the bank’s internal loan-to-value ratio being fallen below or even the mortgage debt no longer being fully covered by the value of the mortgage. In this context, the development of loans where credit was provided outside bank guidelines (exception to policy [ETP]) is an important element of risk assessment. The ETP criteria need to be carefully chosen and applied in a stable manner so that the bank’s board of directors has a transparent view of the mortgage portfolio’s risk exposure that is comparable over time. According to FINMA analyses, most of the ETP financing stems from exceeding bank affordability limits. Prudent institutions are responding to the heightened risk situation in the investment property segment and reviewing possible countermeasures, for example reducing the loan-to-value ratios, a shorter repayment period, more frequent requests for the table of tenants or regional changes to capitalisation rates. The various risks have to be assessed by segment and region, especially for steering the mortgage portfolio or when critically reviewing estimated values. Affordability risks in the mortgage port- folio need to be closely monitored and the ETP criteria must be aligned to the institution’s risk tolerance. Best practice requires that a bank is able to monitor the development of its ETP positions in new and established business for each segment in a standardised form.

Mortgage risks for banks

FINMA has been paying close attention to developments on the mortgage market for a number of years. Regulatory audit firms periodically assess the mortgage risks held by banks and review lending procedures. Through supervisory on-site reviews, supplemented by occasional stress tests at specific institutions, FINMA has been able to form its own opinion about the practice in mortgage lending among the supervised institutions. In order to better assess the risk of banks in the mortgage-lending market, FINMA took additional steps during the reporting year. In particular, it conducted more onsite supervisory reviews lasting several days and shorter deep dives at over twelve banks. Institutions were requested, on the basis of these findings, to initiate improvements in relevant areas including internal directives, criteria for granting loans, regulation of competencies and risk management. Moreover, a survey of residential mortgages was conducted, which covered over 35 institutions. The results show that banks use the room for manoeuvre granted by the SBA in its self-regulatory guidance on residential mortgages to a different extent. In particular regarding the affordability of loans a great variety of practices and criteria could be identified among banks. On the other hand, the more narrowly defined repayment criteria of the SBA guidance result in more standardised behaviour.

FINMA also created its internal technical capacity requirements in order to make standardised evaluations as regards developments in the granting of new mortgages by larger institutions. A further significant measure was a mortgage stress test conducted in the fourth quarter and involving 17 banks. The test was designed to acquire a better understanding of the banks’ susceptibility and capacity to absorb increased losses from the mortgage business. The stress test was based on information provided by the banks on the loan-to-value ratios as well as the affordability and maturity profiles of their mortgage portfolios. This snapshot of many banks under the same stress test conditions provided FINMA with an informative and comparative analysis of the asset portfolios and served to identify outliers.

FINMA may demand additional equity capital if it concludes that the minimum capital requirement and capital buffer do not provide adequate protection given an institution’s risk profile. It has already used this measure in a number of instances and it will continue to monitor the situation at further banks. With all the supervisory tools at its disposal, FINMA is thus equipped to respond to entity-specific risk conditions. However, these targeted entity-specific measures are not suitable for mitigating heightened risks in the mortgage market as a whole, or even segments of it. That requires changes to the regulatory framework. Options include, for example, changes to banks’ self-regulation, adopting more prudent criteria for residential lending or a revision of the equity capital requirements as set out in the Federal Council’s Capital Adequacy Ordinance (CAO) in order to sufficiently account for the increased risk exposure of residential investment property financing. It has to be considered that, overall, the value adjustments for default risks have steadily fallen in recent years. At the end of 2017 the value adjustment ratio for mortgage receivables across banks was just 0.2%.

(From the Annual Report 2018)