Self-regulation in Swiss financial market law

The different types of self-regulation

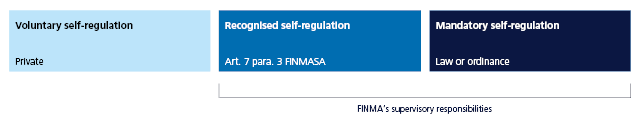

FINMA distinguishes between three types of self-regulation:

- voluntary self-regulation on a private, autonomous basis without state involvement

- self-regulation recognised as a minimum standard

- compulsory self-regulation

Recognition as a minimum standard

Article 7 para. 3 FINMASA allows FINMA to recognise self-regulation as a minimum standard and to use its supervisory powers to enforce this. These standards then apply not only to members of the self-regulatory organisation (SRO), but also to all other organisations in the sector.

For the recognition of self-regulation as a minimum standard, in particular, FINMA will ensure that this is broadly based. Self-regulation will be recognised by FINMA’s Board of Directors.

FINMA calls on the self-regulatory associations also to observe the fundamental aims of the regulatory requirements placed on FINMA. If the content of a self-regulation is of significant material significance, FINMA may also provide for public consultation.

Approval of compulsory self-regulation

The legislator tasks the SROs with compulsory self-regulation on specific issues. Mandates of this type are to be found in the Banking Act (Art. 37h, Securing of deposits) and the Anti-Money Laundering Act (Art. 24 ff AMLA). FINMA’s approval is required for compulsory self-regulation.