Digitalisation in the financial sector

FINMA once again dealt with numerous practical questions in the area of cryptoassets in 2023 and ensured compliance with applicable law, in particular for the protection of clients. It also set out its supervisory expectations in the area of artificial intelligence in line with its strategic goals.

Technology-neutral assessment of practical questions concerning cryptoassets

The interest in cryptoassets remains high among both new market participants and established financial institutions. FINMA responded to all corresponding enquiries on the basis of the applicable law. The trading and custody of payment tokens and staking were the core topics of interest in 2023.1 An initial application for licensing as a distributed ledger technology (DLT) trading facility was in progress. FINMA also participated actively in the regulatory project for the successor to the FinTech licence.

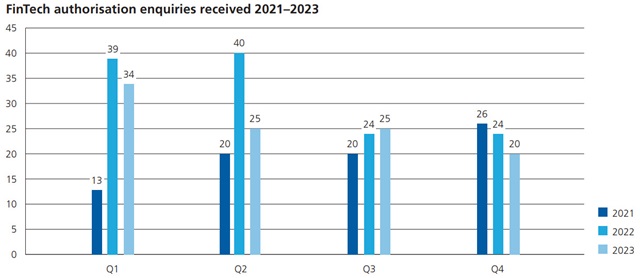

Swift processing of FinTech authorisation enquiries

FINMA received around 100 FinTech authorisation enquiries in 2023, which is roughly the same number as in the previous year (see chart below). FINMA was able to process these enquiries swiftly by providing sufficient resources with a high level of expertise. This enabled it to process FinTech enquiries within an average of two months in 2023. The actual processing time in each individual case depended largely on the complexity of the project and the quality and degree of detail of the enquiries. Clear and consistent factual information, for instance concerning technical details, the allocation of responsibilities and the economic background, facilitates the assessment of a project. The projects submitted varied greatly in terms of content. However, they generally bore reference to current trends in the FinTech sector, such as decentralised finance, the tokenisation of assets and the use of tokenised items in a metaverse.

Stable interest in crypto activities of institutions supervised by FINMA

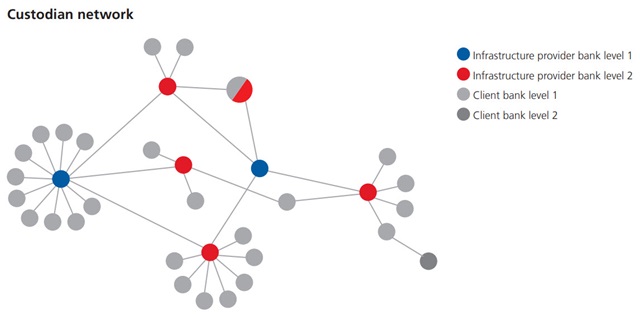

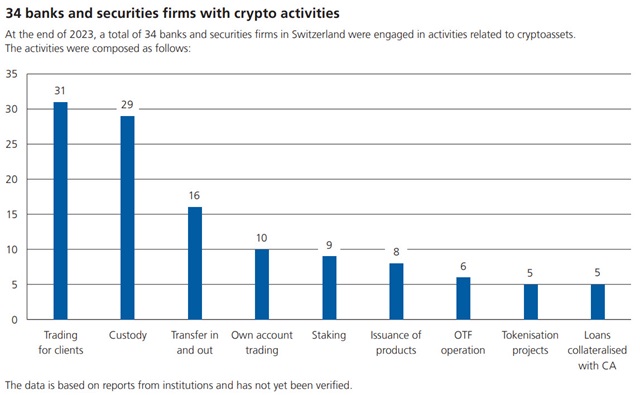

The number of FINMA-supervised institutions offering services in the crypto sector rose slightly in 2023 compared to the previous year, from 30 to 34 banks and securities firms, despite the fact that the market for cryptoassets had bottomed out at a lower level in 2022 following various scandals. FINMA dealt with various issues in this connection while taking into account the risks posed by the dynamic developments in this area. In February 2023, it introduced standardised reporting processes for activities with cryptoassets. The reports indicate that cryptoassets (almost exclusively payment tokens) amounting to around CHF 6 billion were held in custody. The bulk of these were client holdings and only around CHF 0.7 billion were own holdings. It also emerged that while the majority of institutions offer custody, they rely on other banks and securities firms as third-party custodians for this. The third-party custodians were found to be highly concentrated among a small number of companies, as shown by the depiction of the custodian network below (red and blue nodes).

The majority of enquiries from institutions supervised by FINMA in connection with crypto activities concerned the trading and custody of payment tokens. The entry into force of the Distributed Ledger Technology Act created a specific legal basis in the Banking Act for segregating payment tokens held in custody for clients in the event of bankruptcy (Art. 16 no. 1bis BA). In order to achieve such a segregation of custody accounts and thus avoid capital requirements, banks must hold the payment tokens in readiness for custody account clients at all times. If they do not keep the cryptoassets in custody themselves, they must ensure that protection under insolvency law (in accordance with Swiss law or a similarly secure legal basis if abroad) likewise exists in the event of a sub-custodian’s insolvency. Owing to the transition of the Ethereum blockchain from a proof-of-work to a proof-of-stake consensus algorithm, questions concerning staking are increasingly gaining in importance.

The questions about staking focus on substantiating the legal interpretation for distinguishing between custody accounts protected in the event of bankruptcy and deposits exposed to the risk of insolvency. These mainly revolve around the central criterion for bankruptcy protection, which is that the cryptoassets are held in readiness for the customer at all times. In Guidance 08/2023, FINMA set out how it intended to treat staking services in view of the current legal uncertainty, on account of which FINMA would review its classification of staking services in the event of any relevant court rulings or international developments.

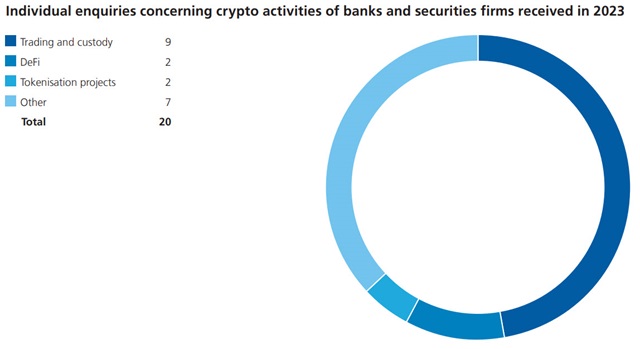

Critical review of enquiries in the area of decentralised finance

FINMA also responded to enquiries in the area of decentralised finance (DeFi) and closely followed developments in this area in 2023. When assessing these enquiries, it drew on the principles of technology neutrality and economic and functional substance (see FINMA Annual Report 2021, page 20). Many allegedly decentralised applications nonetheless turned out to be controlling operators, so that there was no genuine decentralisation. Indications of a type of control relevant under financial market law arose, for instance, from the management of the further development of applications. For example, the operator would have admin keys, or hold the majority of governance tokens, or the application would be dependent on data entered by a specific person, e.g. via an oracle. Other indications were business relationships with end users and income flows from the application to a specific person.

First application for licensing as a DLT trading facility

A new financial market infrastructure, the DLT trading facility, was launched with the entry into force of the DLT Act on 1 August 2021. In particular, FINMA established that DLT trading facilities may also offer possible settlement services to third parties, i.e. not exclusively to participants in their own trading facility. FINMA has since conducted a large number of meetings with potentially interested parties concerning this new licensing category. It received the first formal licence application for a DLT trading facility in the year under review. The project will offer trading and post-trading services and ensure the smooth delivery of DLT securities against payment (delivery versus payment) in an ecosystem with limited access by means of a smart contract on a public blockchain.

(From the Annual Report 2023)