How does FINMA guarantee proportionality in its supervision?

First and foremost, the supervised institutions themselves bear responsibility for good leadership and adequate risk management. Those who follow the rules, or who have a well-structured risk management framework, are less likely to be subject to intensive supervision.

FINMA carries out the most intensive checks on those financial service providers whose size and complexity pose the greatest risk potential for the financial centre and its customers. It steps up its checks on large banks and insurance companies, with direct contact to the board of directors, executive board and other key organisational units.

In the case of large supervised institutions, FINMA monitors the requirements relating to capital, liquidity, risk management, compliance and the existence of independent control bodies, mostly through on-site inspections. It also examines the broader requirements for ensuring operational resilience as well as climate-related financial risks and their impact on business strategy, business model and financial planning.

However, supervision of smaller institutions with a lower risk is largely data-driven, with less extensive reporting requirements and less on-site inspections both in absolute and relative terms. Supervision of these institutions is only intensified if there are signs of increased risk.

Small, well-managed and stable institutions – for example the 56 institutions that take part in the small banks regime – also benefit from regulatory relief and fewer direct checks.

-

On-site inspections

-

FINMA ensures, through its supervision, that rules are followed. To achieve this, it is increasingly reliant on its own on-site inspections, the number of which has been continuously increasing in recent years. However, its approach has been proportional, as the following graphs and tables show.

Initially, the number of on-site inspections grew during the period from 2013 to 2025. In absolute figures, category 2 and category 3 banks had the most on-site inspections.

Source: Own calculations

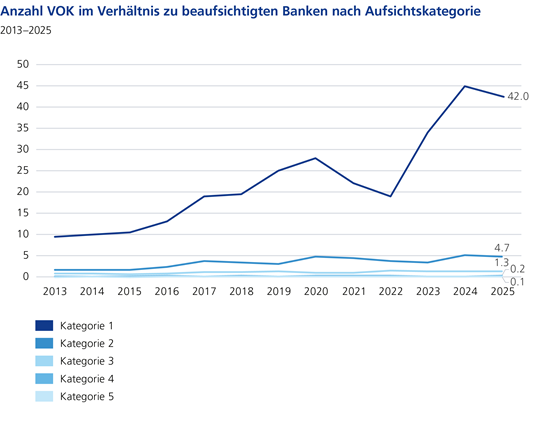

If we consider the number of on-site inspections relative to the number of institutions in the respective categories, we can see that banks in supervisory category 1 had disproportionately more on-site inspections than those in categories 2 and 3. The smallest institutions, i.e. the institutions in supervisory categories 4 and 5, were visited the least, relatively speaking. In other words: UBS, for example, has over 40 on-site inspections per year, whereas a small bank is only subject to an on-site inspection every 8-10 years on average.

Source: Own calculations

However, it is not only the size of an institution that is important, but also its potential risk. This is reflected internally at FINMA with a risk rating of high/medium/low. A comparison of the ratio of on-site inspections carried out at banks with a rating of low, compared to institutions rated medium and high shows in the following graph that in the last 13 years significantly more on-site inspections have been carried out on banks with a worse rating. The factor in the graph indicates the ratio of on-site inspections at institutions with a risk rating of medium/high compared to those with a risk rating of low. In 2025 the factor was 12, which means there were 12 times more on-site inspections carried out at institutions with a risk rating of medium/high than there were at institutions with a risk rating of low. This risk-oriented approach to supervision has been strengthened in recent years.

Source: Own calculations

Similar results are obtained when considering the institutions in the fields of insurance and asset management.

-

Enforcement proceedings

-

FINMA also applies enforcement in a proportionate manner as a visible means of sanctioning breaches of supervisory law and restoring order.

These enforcement proceedings may be conducted against licence holders and their employees, against unauthorised financial services providers and against any participants in the Swiss financial market. In 2025, FINMA concluded a record 55 enforcement proceedings.

Source: Own calculations

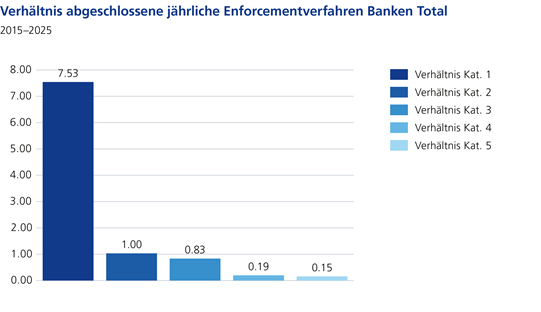

In the last ten years, FINMA has, on average, initiated significantly more enforcement proceedings against large institutions than smaller ones.

Source: Own calculations