Climate risks and other nature risks faced by financial institutions

Nature risks, including climate risks, may be significant for Swiss financial institutions. For banks, asset managers and insurers, the sources of risk generally lie in the physical impacts of changes in nature, such as climate change, or in transition risks, for example as a result of far-reaching climate policy measures. For example, assets in affected economic sectors on the balance sheets of financial institutions could become illiquid or be exposed to increased valuation risks. In principle, climate-related and other nature-related financial risks can be classified and captured in the traditional risk categories, such as credit, market, insurance or operational risks. As such, this is not a new risk category, but a risk driver. However, these risks give rise to specific challenges due to their particular characteristics.

In its supervisory practice, FINMA follows the definitions and recommendations of international standard-setting bodies such as the Basel Committee on Banking Supervision (BCBS), the International Organization of Securities Commissions (IOSCO), the International Association of Insurance Supervisors (IAIS) and relevant guidance and recommendations by the Central Banks and Supervisors Network for Greening the Financial System (NGFS).

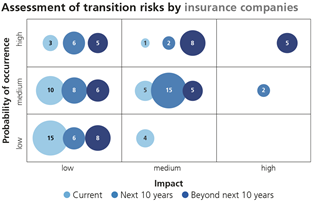

Transition risks

For transition risks, the focus is on the transition to a low greenhouse gas-emitting society. Climate policy measures or technological breakthroughs relevant to climate change mitigation can generate significant indirect risks of various kinds for financial institutions. For example, a financial institution may be invested in a company (market risk) or extend loans to a company (credit risk) that is unable to keep pace with political measures or technological developments. Other possible risks are legal risks arising from corporate misconduct, as well as from changes in case law, abrupt shifts in the behaviour of market participants and the resulting reputational risks for the financial institutions concerned.

According to FINMA surveys conducted in 2025, banks and insurers currently assess transition risks for the Swiss financial centre as relatively low, but expect them to increase over the next ten years:

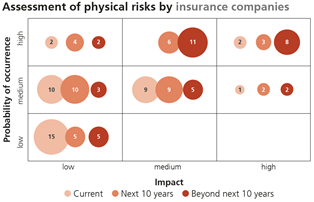

Physical risks

In the case of physical risks, a general distinction is made between acute and chronic risks. Acute risks focus on event-driven incidents, such as storms or floods. Chronic risks mean longer-term impacts, such as rising sea levels. These risk drivers can result in losses for financial institutions through traditional risk categories (e.g. credit and market risks), including unanticipated losses.

In their assessment of physical risks, banks and insurers also expect a clear increase over time:

FINMA shares the assessment of financial market participants that exposure to transition and physical risks will increase in the future. However, there are still major uncertainties in the modelling of climate risks. Physical risks in particular may still be underestimated.

Further information on the assessment of climate-related financial risks for the Swiss financial centre can be found in FINMA’s annual climate risk reports (pursuant to Art. 40d CO2 Act).