Financial technology and digitalisation (2016)

Innovation is an important part of maintaining competitiveness in the Swiss financial centre and ensuring it is equipped for the future. In fact, innovation is a must if the financial market is to maintain its dynamism and capacity to develop. FINMA is in contact with a broad range of stakeholder groups related to FinTech and constantly reviews the new challenges presented by technological advances. For instance, FINMA has a direct information and contact channel to deal with FinTech-related issues.

Switzerland shows continued interest in FinTech

FINMA reported on the growing FinTech trend in its 2015 Annual Report. The Swiss financial sector’s interest in digitalisation has continued to grow in the interim. FINMA has seen a rise in new service offerings in the business-to-business segment (B2B) and the business-to-customer segment (B2C). The volume of FinTech-related research initiatives, support programmes and start-up companies has also increased. FINMA has kept abreast of the latest developments through regular dialogue with experts, companies and associations.

FinTech desk

FINMA has taken organisational steps to adjust to the new market situation. It responded to a request from the FinTech sector at the end of 2015 for a centralised channel to access relevant information by setting up the FINMA FinTech desk, which became operational at the beginning of 2016. It manages all FinTech-related enquiries and it has the expertise to provide rapid and targeted answers. Interested members of the public or individuals working for startups or established financial services providers can obtain information about legal issues relating to the financial market via a dedicated FinTech desk.

Technology-neutral regulation case study: identification of new clients (digital onboarding)

FINMA maintains a technology-neutral approach to its regulation. Supervisory law must adopt a neutral position regarding technological developments and business models, i.e. neither facilitate nor hinder them. However, that does not mean the requirements applied to the provision of digital services have to be identical to those for analogue service providers. More importantly, the purpose of a regulation – one limiting the risk of money laundering, for example – must be upheld irrespective of whether market participants offer analogue or digital services. By defining the rules governing the digital verification of identification documents in Circular 2016/7 “Video and online identification”, FINMA established the conditions for identifying clients through the internet when initiating a business relationship.

As tangible documents cannot be sent via the internet, FINMA set out the necessary technical requirements to establish a business relationship, for example the optical recognition of security features by video chat. Video identification is equivalent to providing identification documents at a counter, while online identification equates to identification through correspondence.

FINMA regulations are technology-neutral

FINMA’s approach to FinTech is based on three principles: consistent technology neutrality, legal certainty and principle-based regulation. FINMA systematically reviews its regulation for market-entry hurdles to technology-based business models. Circular 2016/7 “Video and online identification” is an example of principle-based regulation; its lean framework allows providers to be flexible in how they structure their services and implement them at a technical level. The Circular thus extended the operating framework to include innovative business models.

FINMA has also authorised the digital conclusion of asset management agreements. FINMA Circular 2009/1 “Guidelines on asset management” had stipulated the need for a written asset management contract. This Circular has been amended and alternative forms of concluding contracts via digital channels are now also legitimate. Procedural requirements under the Collective Investment Schemes Act remain reserved. The changes came into force on 1 August 2016.

FINMA’s commitment to progressive operating conditions for FinTech companies

Switzerland also needs to adapt its overarching legal framework to consistently improve the operating environment for FinTech. FINMA has conducted in-depth discussions with the FinTech sector and representatives of established financial service providers to identify obstacles within the supervisory framework conditions. The main barriers to FinTech stem from banking legislation. FINMA also performed a benchmarking exercise against other financial centres and their FinTech initiatives. Against this background, FINMA proposed the creation of an effective and forward-looking legal regime. The aim here is to amend the Banking Act based on two pillars: the extension of the licence-free area (sandbox) to work with innovative business models free of any bureaucratic constraints, and a new licensing category tailored to established FinTech companies not involved in any conventional banking business and which, as a result, do not need to be regulated in the same way as banks. In view of the reduced risk, the authorisation requirements can be less exacting than with a traditional banking licence. The proposed licensing procedure would significantly lower the entry barriers to providers of payment systems, digital asset management applications and crowd platforms, particularly with respect to capital, corporate governance and risk management requirements. The rationale behind the approach is to simplify current regulations as opposed to adding more regulation.

The Federal Council has received and advanced FINMA’s proposals. The consultation process to review banking legislation will begin in early 2017.

International engagement

The topic of FinTech is also the subject of extensive discussion at the international level. FINMA is committed to making Switzerland an internationally competitive FinTech location. In 2016, FINMA joined the international FinTech debate and strengthened cooperation with other foreign supervisory authorities in digitalisation and financial technology. On 12 September 2016, FINMA signed an agreement to deepen FinTech cooperation with the Monetary Authority of Singapore (MAS). FINMA plans to conclude further cooperation agreements in 2017.

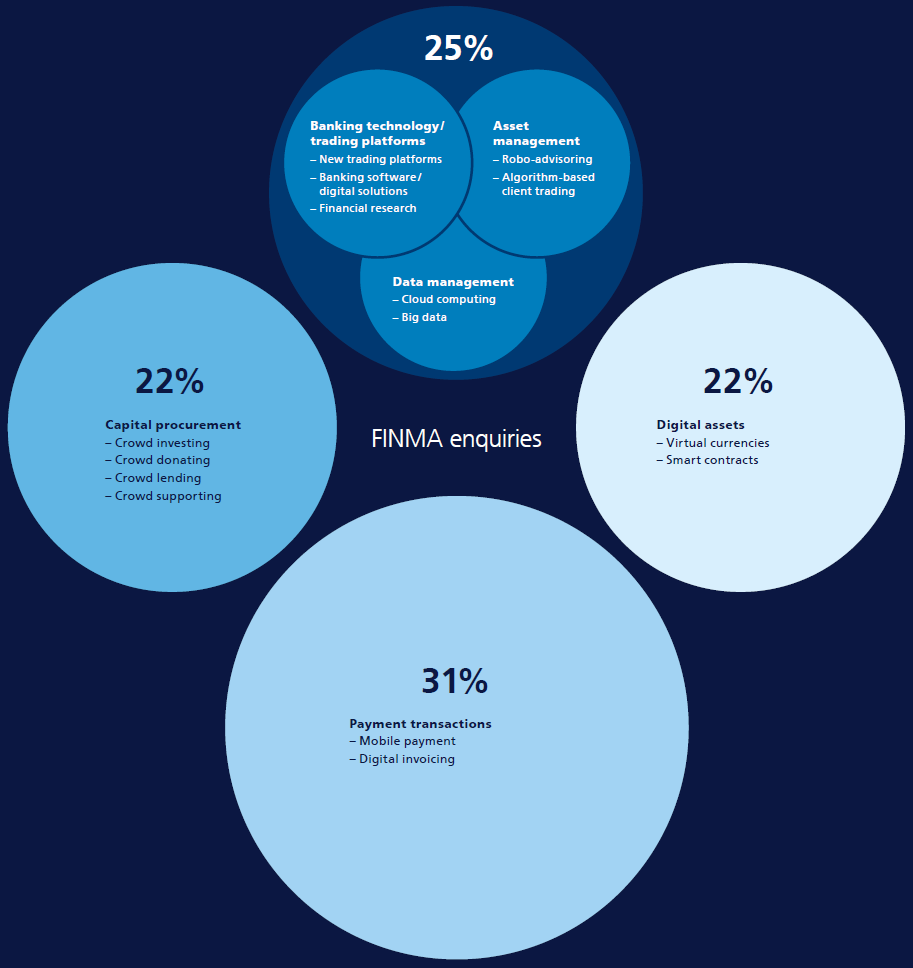

FinTech enquiries handled by FINMA

FINMA has seen a steep rise in the number and variety of FinTech business models, which in Switzerland now cover payment transactions, virtual currencies, capital procurement, asset management, banking technology/ trading platforms, insurance and data management. FINMA received approximately 270 FinTech-related enquiries in 2016, mainly about capital procurement (22%), payment transactions (31%) and virtual currencies (22%).

(From the Annual Report 2016)