In a report published today, the Swiss Financial Market Supervisory Authority FINMA provides a detailed assessment of the recovery and resolution plans of the systemically important Swiss institutions. FINMA views the Swiss emergency plans of Credit Suisse and UBS as effective. The emergency plans of PostFinance, Raiffeisen and Zürcher Kantonalbank, however, do not meet the statutory requirements yet.

The two large Swiss banks were required to submit effective emergency plans for their systemically important functions in Switzerland by the end of 2019. Hence FINMA is publishing a report at this juncture setting out the progress that has been made by all the systemically important Swiss institutions in recovery and resolution planning (see the glossary below for an explanation of the relevant terminology).

FINMA CEO Mark Branson comments: “Implementation of the Swiss too-big-to-fail regime is critically important to the stability of the financial centre. Our report on recovery and resolution planning is designed to create transparency about where we stand with regard to implementation. We are well aware of the hard work that all the institutions involved have put into this issue. Considerable progress has been made, but there is still more to do.”

Recovery plans approved and the large banks’ Swiss emergency plans are effective

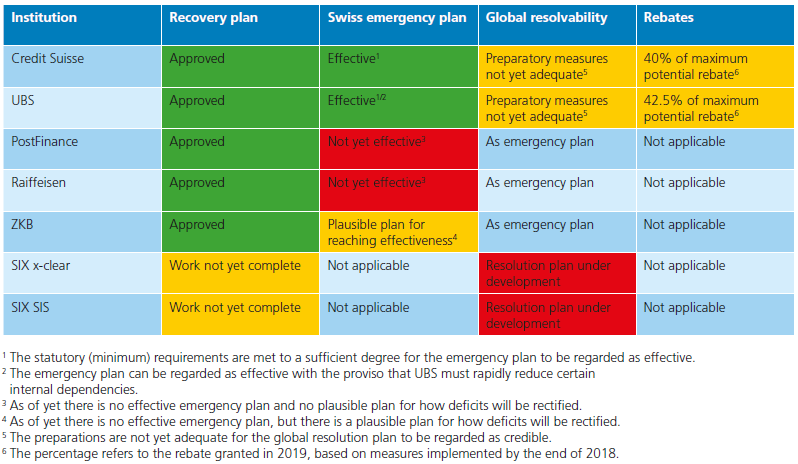

All five systemically important Swiss banks have submitted recovery plans to FINMA. FINMA has approved all of these plans. In addition the two large Swiss banks were required to produce effective emergency plans for their Swiss operations by the end of 2019. FINMA has reviewed these. In the case of Credit Suisse FINMA regards the emergency plan as effective. UBS is also judged by FINMA to have met the requirements for an effective emergency plan, with the qualification that certain joint and several liabilities remain excessive.

The three domestic systemically important banks have also submitted an emergency plan, but were at different stages of implementation at the end of 2019. None of the plans is deemed to be effective yet. At Zürcher Kantonalbank there is a plausible plan for how the capital and liquidity resources required in the event of a crisis can be built up further. Raiffeisen and PostFinance do not yet have plausible plans for accumulating the necessary gone concern funds for recapitalisation in a crisis. All three domestic banks have work ongoing to develop an effective emergency plan.

Global resolution plans and the rebate process

FINMA is required to draw up a global resolution plan for the two large banks. Unlike the emergency plan, which relates purely to the banks’ systemically important functions in Switzerland, this global resolution plan covers the entire banking group worldwide. FINMA assesses this global resolvability on the basis of whether the preparations of the large banks are sufficient to successfully implement the resolution plan if necessary. It has concluded that both banks have already taken important preparatory steps and have thus made considerable progress with respect to their global resolvability. In particular, FINMA believes the requirements for structural disentanglement are now fulfilled. For instance, the two banks have created holding structures and Swiss subsidiaries to facilitate this disentanglement. In other areas, particularly with regard to funding in resolution, further implementation work still needs to be done. It should be taken into account that the regulatory requirements have not yet been published in this area. Since the domestic systemically important banks have little or no foreign business, their resolution plans relate solely to the systemically important functions in Switzerland. They are therefore largely interchangeable with the emergency plans.

The supervisory assessment of the large banks’ global resolvability has a direct impact on the annual rebate process. FINMA can grant the large banks relief on certain capital requirements if they have improved their global resolvability and the required measures have been predominantly implemented. As in recent years, FINMA identified a number of such improvements in 2019. This has led to Credit Suisse utilising 40% of its maximum rebate potential and UBS 42.5%.

Financial market infrastructures: recovery and resolution planning under way

Systemically important financial market infrastructures are also required to prepare a recovery plan detailing the action they would take to ensure their stability on a sustainable basis in a crisis, so allowing the continuation of their systemically important business processes. Both financial market infrastructures designated as systemically important in Switzerland (SIX x-clear and SIX SIS) have recovery plans in place. The plans have been continuously improved, but due to the high standards for these plans further improvements are needed before they meet the conditions for approval. FINMA has also commenced work on developing resolution plans for SIX x-clear and SIX SIS.

Overview of the progress of work (as at the end of 2019)

Transparency on the Swiss too-big-to-fail regime

FINMA publishes information on its assessment of the emergency plans in a report. The report creates transparency about the progress that has been made by the systemically important banks in their emergency planning. The report also looks at the too-big-to-fail regime in Switzerland generally, FINMA’s role in the event of a resolution, the primary resolution strategies of the systemically important banks as well as the current status of recovery and resolution plans at the financial market infrastructures.

Glossary

| Recovery plan | In the recovery plan, the systemically important institution sets out which measures it will use to ensure its stability on a sustainable basis in the event of a crisis and be able to continue its business activities without government intervention. FINMA is responsible for reviewing and approving the recovery plan. |

| (Swiss) Emergency plan | Systemically important banks must demonstrate in the emergency plan that their systemically important functions can be continued without interruption in a crisis. Only functions that are critical to the Swiss economy are deemed systemically important, which includes in particular the domestic deposit and lending businesses as well as payment services. Thus it is sometimes referred to as the Swiss emergency plan. FINMA reviews the measures in the emergency plan with regard to their effectiveness if the bank were at risk of insolvency. |

| Resolvability | Resolvability refers to a company’s ability to be resolved in an orderly manner. A systemically important bank is deemed resolvable if conditions are in place that would allow it to be restructured or liquidated in the event of a crisis without endangering financial stability. |

| Resolution plan | The plan drawn up by FINMA to restructure or liquidate a systemically important institution in its entirety (in the case of an international systemically important bank the entire group, including foreign group entities, which is why this plan is also referred to as the “global resolution plan”). In this plan FINMA sets out how the restructuring or liquidation would be carried out. |

| Rebates | The Swiss too-big-to-fail legislation contains an incentive system under which the two large Swiss banks are eligible for rebates on their gone concern capital requirements in return for improvements to their global resolvability. |

Contact

Tobias Lux, Media Spokesperson

Phone +41 (0)31 327 91 71

tobias.lux@finma.ch

and

Vinzenz Mathys, Media Spokesperson

Phone +41 (0)31 327 19 77

vinzenz.mathys@finma.ch